All the surveys indicate growing take-up of FX algos among corporates and the real-money community. But aren’t they the cautious ones? William Essex wonders how today’s regulatory environment could possibly be a good time to try a new approach to transacting.

Strategy backtesting is a mix of art and science. Quants who rely too much on patterns in data will fall victim to curve fitting, while others create theories to fit their models. Here are leading quants’ perspectives on best practice in strategy backtesting: by Jared Broad of QuantConnect.com

All the building blocks would seem to be in place for the take-up of algorithmic forex trading by the buy-side in the Nordic region, and yet it is still very much a work in progress as Adam Cox discovers.

Markets are constantly changing, and modern markets are changing very quickly, sometimes more quickly than traders are able to adjust their methods to these changes. No wonder that within this new reality the demand for robust trading strategies becomes predominating, and therefore the importance of methods that allow to adequately assess the robustness rises dramatically: By Alexey Krishtop, Managing consultant at Edgesense Solutions Ltd.

Canada has a tight-knit financial community, a strong focus on best execution and a degree of sophistication not often found in other markets. These factors taken together mean that algo usage is gradually coming on stream. Meanwhile, the competition among providers is fierce.

In the fragmented, fast-moving world of foreign exchange, there are plenty of arguments to be made as to how algorithms can give the buy-side a helping hand in sourcing liquidity, reducing signalling risk and keeping market impact to a minimum. Yet to date, the bulk of the real money has been following a more traditional approach when it comes to execution.

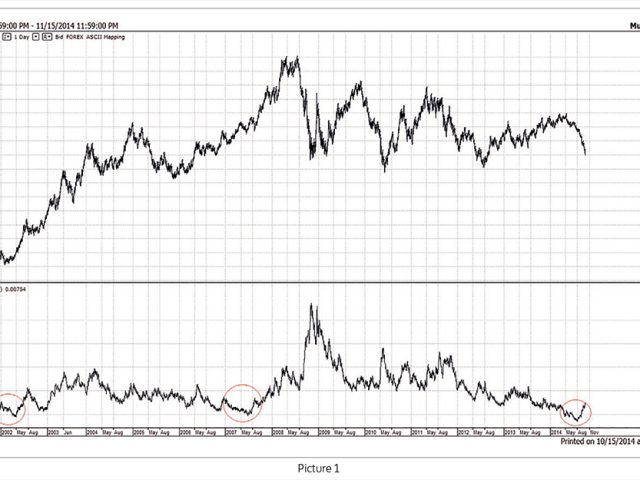

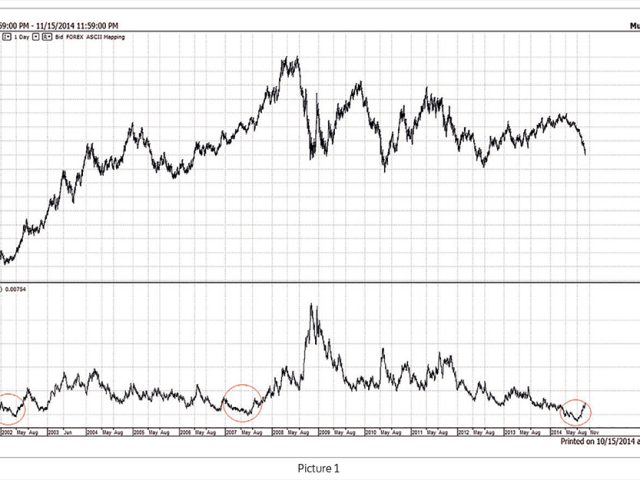

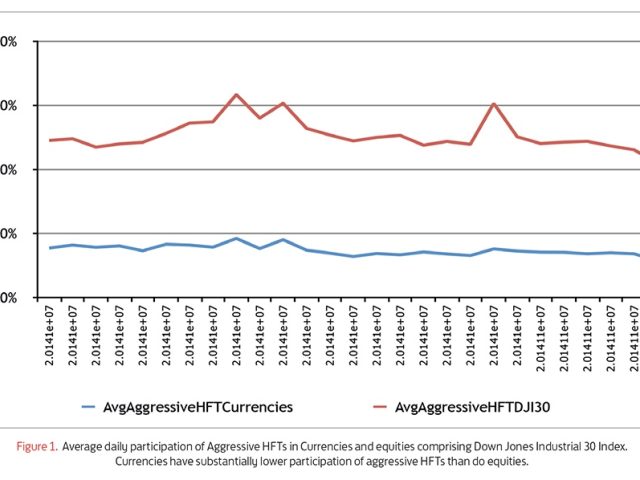

The prevalence of aggressive high-frequency trading activity can be measured and our latest research shows striking differences by asset class. Understanding the proportion of aggressive high-frequency traders in the markets at any given time helps traders dramatically improve their trading performance.

Switzerland, with its tradition of avoiding conflict and its idyllic mountain scenery, tends to be thought of as a rather peaceful country. After 14 January 2015, it is hard to imagine anyone in the markets still thinks of Switzerland as a place of calm.

By developing an algorithmic trading platform that offers different trading strategies through a single interface, TD Securities is hoping that TD OpenICE will appeal to the growing number of institutional clients trading FX electronically. We talk to Paul Aston, head of Quantitative and Algorithmic Solutions, about the importance of simplicity and transparency.

Algorithmic execution has come a long way in foreign exchange, but it is still largely confined to the spot market, despite rising demand for forward algos. Joel Clark reports.