Algo execution is intimately linked to the growth of the number of venues, says Carlos Gomez Gascon, Executive Director at JPMorgan. He adds that FX market fragmentation has made it more efficient to access overall market liquidity with the help of an algo, with fragmentation particularly high on the most liquid instruments, meaning that early FX algo demand was concentrated in the G7 currency pairs. “Real money and systematic funds were the early adopters of algos and they drove innovation to support more complex execution offerings,” Gascon explains. “Hedge funds and banks later followed suit to enhance their access to prices as liquidity continued to become less concentrated on interbank venues. We now see corporates adopting algos at higher rates because execution transparency supports their fiduciary responsibility.”

Tom Appleton, Executive Director, FX Algorithmic Execution at Crédit Agricole CIB, generally agrees, adding that the initial growth was in G10 because providers did not have experience in building algos for less liquid pairs. “Yet as algo FX trading evolved and liquidity grew on electronic platforms, clients saw a major benefit in emerging market (EM) deliverable pairs as well,” he says. “In Europe there is a very mixed picture, with algo uptake in certain countries happening much more quickly than others, with those countries that use e-FX more than voice typically adopting algos earlier.” Now however, he believes there are a number of opportunities in the market for further expansion. Appleton explains: “The corporate space is really exciting at the moment and we are seeing some very large tickets from our corporate clients. The feedback has been great; we have an experienced team and being able to help our clients through an execution, partnering with them to not only achieve some really great cost savings, but explaining what’s happening in the market, has really engaged them with the product.”

This pattern of corporate adoption is global but is particularly evident in the US/UK and Europe, he argues, while NDF algos are also in constant demand from the buy side and Appleton believes that this is perhaps the most important area of expansion for the bank from a product perspective. “The buy side will continue to look at ways to lower execution costs and develop electronic solutions,” he says. “NDFs are one of the areas that will become more electronified and algos will play a greater role as a liquidity source.”

Areas ripe for expansion

Commerzbank has also began to see larger corporates start to transition to using FX algos around three or four years ago, particularly those with their own dedicated execution desks.

In continental Europe, although the majority of the bank’s corporate clients have definitely heard about algo execution, not all of them have realized the full potential of FX algo trading yet, says Nickolas Congdon, Director and Head of e-Trading Services at Commerzbank. However, he believes that clients are increasingly smarter in terms of their order execution. “They’re becoming more comfortable using an advanced order and that’s because they’re asking the right questions now, such as how does Commerzbank manage the different liquidity sources in what is a very fragmented market,” Congdon adds. “They’re also increasingly asking us how they can minimise their execution footprint and better understand the metrics around what we are providing. We’ve seen promising results with our clients, especially the corporate clients, as they become more interested in gaining visibility and finding efficient ways to better evaluate their FX exposure.”

According to Congdon, EM pairs are also a key opportunity for growth and is an area the bank has been very successful in, with its EUR/CNH ranking in the top 3 on a major third party platform for algo volume year-to-date, for example.

Yet leading providers need to understand that the key to meeting rising demand is through the development of more efficient algos, he warns. “With the fast pace of development in technology, we have to continue to innovate if we are to stand out from the crowd,” Nuti explains. “As an example, we have just launched our new Principal Interest algo. Being at the cutting edge of industry developments allows us to continue meeting the ever more sophisticated needs of our clients.”

EM pairs offer the biggest area for further expansion in algo usage, according to Gascon. A good example of it are Asian NDFs where JPMorgan rolled out during 2019 the first algo strategies. Currency pairs where spreads are wide could be an interesting opportunity to reduce transaction cost through the use of algos. In addition, some of the classic EM currencies are now greatly evolved. “Take CNH as an example. Not so many years ago, it was considered quite an esoteric currency to trade. Yet today, looking at market volume rankings per ccy, CNH is on the top 5/top 7. MXN has exhibited significant growth worth mentioning too,” Gascon says.

Responding to demand

Algo execution is also an effective tool for automation. As such, Gascon believes the market will see further growth across less developed instruments such as NDFs, forwards, swaps and options. Then as the instrument base of algos expands, he argues it will become possible to create cross asset products, for example, hypothetically a client in the future might want to automate the instruction buy 10M EUR/USD and 10 oz of gold if UST 10Y moves down 1 bps. In addition, this increased instrument availability is likely to unlock potential from markets in APAC who are used to operating in less electronically developed products, according to Gascon. In terms of how FX algo providers should position themselves to meet growing demand, Gascon believes they would do well to remember that the evolution of algos has always been closely related to market fragmentation and liquidity availability. “As the focus continues to be on liquidity, internalisation will become a key differentiator between different providers to both lower the execution costs and increase liquidity access,” he says.

Although the increase in algo demand has followed a time of expansion in terms of control and customisation for clients resulting in an explosion of optionality in terms of order types and parameters available, Gascon expect that the natural next step will actually be in the opposite direction. He explains: “This is due to at least two key factors. Firstly, it is very hard for clients to gather enough data to verify performance on all possible parameterisations. Clients will lean on their provider’s expertise to optimise execution. Secondly, new users tend to prefer simpler offerings and providers are encouraged to widen their client base.” Yet the only way to achieve greater simplicity is by providing transparent tools to enhance algo visilbility to inform client’s execution decisions. “Full lifecycle products, such as JPMorgan’s Algo Central which encompasses pre- and post-trade and real time analytics, are a must have in the product offering,” says Gascon.

Evolving the TCA market

While the market is growing, the space is simultaneously becoming increasingly competitive. New entrants have recognised that traditional voice business is shifting, and will continue to shift, towards algo execution, Appleton explains. “However, just having an ‘algo’ is not enough – it’s a continuous arms race and you need an edge,” he warns. “To stand out, leaders are building value add products directly into third-party platforms, or developing new strategies using the latest AI techniques. The bar is being continually raised and what were once unique selling points are quickly becoming core requirements.” A further key area of growth is that of TCA, which is not necessarily only being driven by increased compliance requirements for greater transparency and reporting. According to Appleton, while bespoke reporting is important for some clients, post-trade integration to third parties is important for others. He adds: “As already mentioned, integration of TCA into third-party order entry screens for pre-trade and real time analysis will be key, as clients increasingly demand deep analysis of their executions and that their TCA provides market/execution details and a tailored breakdown of the order.”

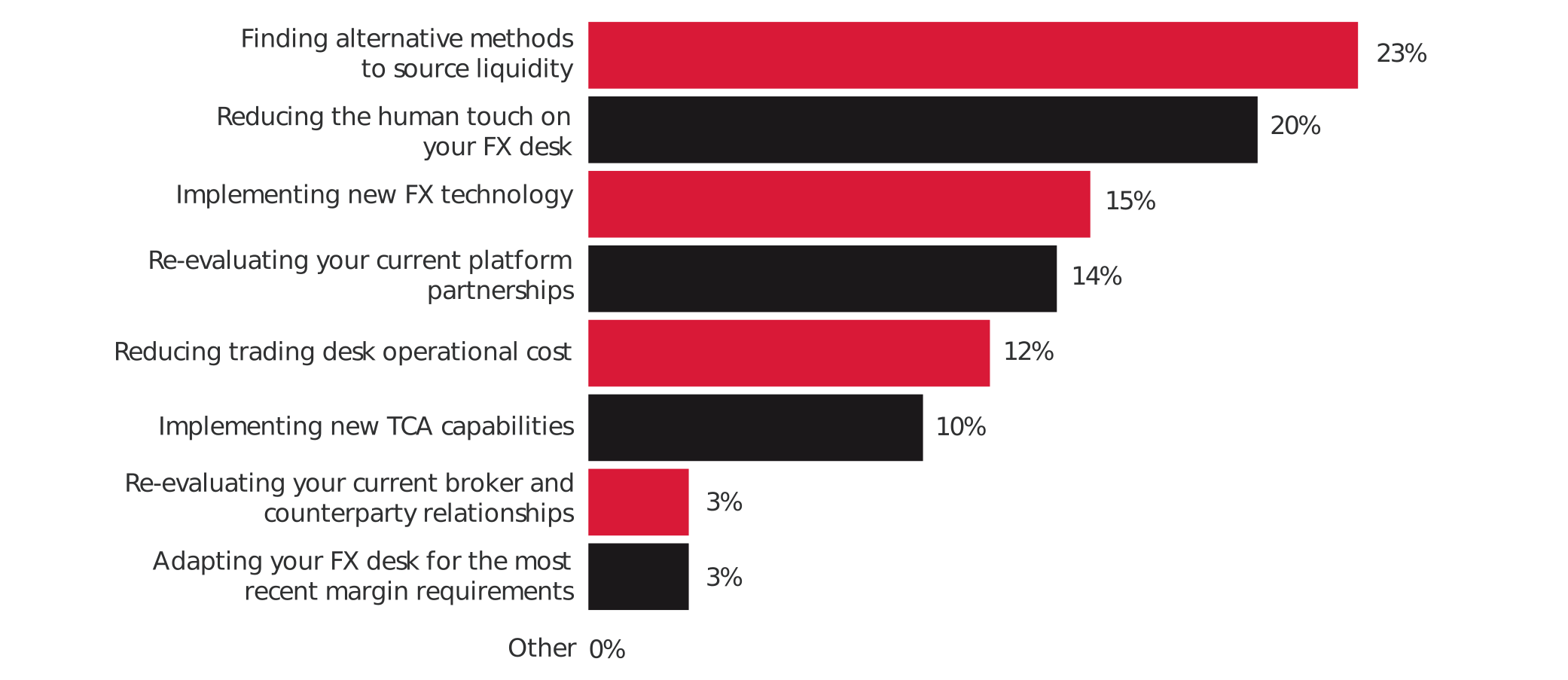

Apart from obtaining best execution for your clients, what is the biggest priority for your FX trading desk?

Better and increased levels of client education would also help to further increase demand for algos, argues Congdon. He explains: “Banks are notorious for over-complicating things. This can lead to dangerous scenarios, especially during periods of market dislocations that the algos had not been adequately trained for. Our focus is on protecting the client and ensuring the algo safety mechanisms are in place to limit the possibility of a suboptimal outcome during these scenarios. There are over 100 different algos in the industry, but they’re all very similar in what they’re trying to achieve. At Commerzbank, we are an advocate for transparency and simplicity. We don’t want to overcomplicate things or make things confusing.”

In addition, Commerzbank’s house business is also driven by algorithmic execution, there are no voice traders, with all new technology developed in-house. “We’re rolling that out to other FX products as well, such as FX forwards, NDFs and swaps which we are algorithmically hedging,” adds Congdon. “As this evolves, we’ll look to offer clients the opportunity to leverage our R&D opposed to going and buying a black box solution from someone else.”

TCA has also risen in importance, partly due to the introduction the FX Global Code of Conduct and best execution requirements under MiFID II, but also driven by client demand for transparency. Clients today should really have a meaningful portfolio of algo executions that they can then use to benchmark against and make better informed execution decisions, says Congdon. “Off the back of that, they can also make an execution policy or an FX policy. We meet with our corporate treasurers and have helped many of them to develop their policies, but in order to do this there needs to be an objective view of the market conditions at the time of the algo execution.”

The reality of machine learning

The industry is likely to see continual evolution in the short to medium term in this space, agrees Nuti. For example, Deutsche Bank’s award winning Market Colour app is recognised across the industry as being a key tool in the growth of TCA, he adds. According to Nuti, the intuitive interface allows the user access to real time data, while the interactive tools in the app enables the user to extract exactly the data they need to make an informed decision.

However, when it comes to the use of next generation technologies, it is vital that clients understand the reason for the use of these technologies so that they feel comfortable in deploying it, he warns. “We embrace the latest advances where there are benefits for our clients. But as noted in AQR’s research paper ‘Can Machines ‘Learn’ Finance?’, the problem with financial markets is that they continuously morph,” says Nuti. “So it’s really important that new technologies can deliver real gains for clients and are not just being implemented for sake of it.”

However, as algo usage picks up, so too does the amount of data available, which is the key ingredient required for the success of AI/ML/quantitative modelling. Therefore the potential is very strong, especially for the largest banks with the most significant amounts of available data, Gascon explains.

Overall, Gascon observes at least three areas of growth in the FX algo space. The first is in order placement optimisation, where clients can set-up the overall expectation of algo behaviour and the algos will attempt to optimise placement given the conditions and boundaries set. A good example of this in the JPMorgan offering is DNA, he adds, which uses cutting edge machine learning techniques, including reinforcement learning and neural networks. The second area would be providing optionality to clients on algos to use before, or during, the execution based on their trading patterns and profile. “The final and last step in terms of technology opportunity might be some sort of autopilot which would take care of the execution given a very high level instruction with few restrictions,” predicts Gascon.

To stand out, leaders are developing new strategies using the latest AI techniques.

Encouraging further adoption

In addition, the trouble with some of the deep learning approaches to AI in trading is the need for consistency with very few errors. So if an AI decides to take a very different course of action to the intent of the user, then this may or may not be perceived well, explains Appleton. “However, that being said, using AI in subroutines that have very specific goals is definitely happening,” he adds. More importantly, according to Appleton there are areas where clients want the traditional FX relationship and where that is working, banks such as Crédit Agricole CIB see no need to change it. “In other areas we are finding there are still clients that can make significant cost and time savings by switching to using algos. This is mostly an education exercise with the client – once they have done a few simple executions, TWAP for example, and been over the TCA, they start to experiment on their own,” he says.

Looking ahead, he expects to see more smaller banks white-labelling the solutions with bigger partner banks where there is client demand for algos but not the appetite to build a standalone execution desk. “We will also see more corporates using algos as they become comfortable executing large tickets sizes with a general uptick in overall volume,” he adds: “In terms of products, we will see more banks marketing AI features and real time diagnostics.” Deutsche Bank also says it takes pride in working closely with its clients in order to ensure they understand the direct and indirect costs of FX execution and other products. “Thanks to the Market Colour app, clients are able to see the tool in action for themselves and are able to see how it works,” explains Nuti. “The functionality in the app demonstrates how the product is designed to save them money on average.”

The bank also provides extensive training on how the tool works so clients feel comfortable using the platform and that they are well supported, which Nuti expects will only further support and encourage greater algo usage going forward. “FX algo trading will continue to be an integral part of a client execution suite,” he predicts. “I envisage continued growth in this space as more investors realise the advantages and this will help ensure that algos remain a core offering in our product line up.”

Meanwhile whilst Commerzbank is developing new algorithmic solutions for both its house and client businesses, at a macro level however, Congdon notes that the market is fluid and clients need to be aware of the impact of new regulation on the market. For example, increased NDF clearing may have an impact on liquidity provision and ultimately the cost of execution.