Christoph you have more than 20 years of international investment banking, trading and management experience. How did you arrive at your current position?

In April 2014 I started here at Union Investment as head of multi-asset trading and looking back at my previous roles, the experience I’ve had across multiple asset classes combined with experience on both the buy- and sell-side has proven extremely helpful in my current role. I actually started back in 1991 in cash equities when I had worked for Dresdner Kleinwort Benson, which at this point in time was one of the leading banks in Germany. Working in the Frankfurt exchange’s trading pit was extremely helpful in terms of developing a true trader’s DNA.

After that I went to J.P. Morgan in London, where I built and ran a proprietary trading team in derivatives for more than six years before returning to run my own hedge fund here in Germany, which was initially part of a larger UK hedge fund company. Here I traded long/short strategies for more than five years. By then I was really involved in all asset classes: cash equities, fixed income and I was also heavily involved in FX trading and derivatives.

Then I moved to working on the sell side for a couple of years which was also extremely important in terms of learning how to combine my experience on the buy-side with the ability to provide client support and coverage at highest levels on the sell-side. This has proven as very helpful in the role I have here at Union Investment as head of multi-asset trading.

Please tell us a little about what your day-to-day job and responsibilities usually involve.

When I joined Union Investment, I expected to become heavily involved in the day-to-day business of trading, which was my key role with my previous employers. But the definition of my role as head of trading for one of the largest European asset managers has turned out to be a different one. I’m running a team of 20 persons and its predominantly about leadership, how to run the team and motivate them to ensure that we deliver the highest value possible to our end investors. Another key part of my role as a manager is about business strategy. What’s about evolution and development of the industry in the next three to five years? What are the big challenges and opportunities we will be faced with and how do we ensure that we stay ahead of the curve? But most importantly, we are a service and solutions provider so how do we assure that we deliver the best value possible and maximise the value we deliver to our end investors and clients?

After joining Union Investment you set about changing the structure of your trading teams to create a consolidated multi-asset trading desk. Why was that?

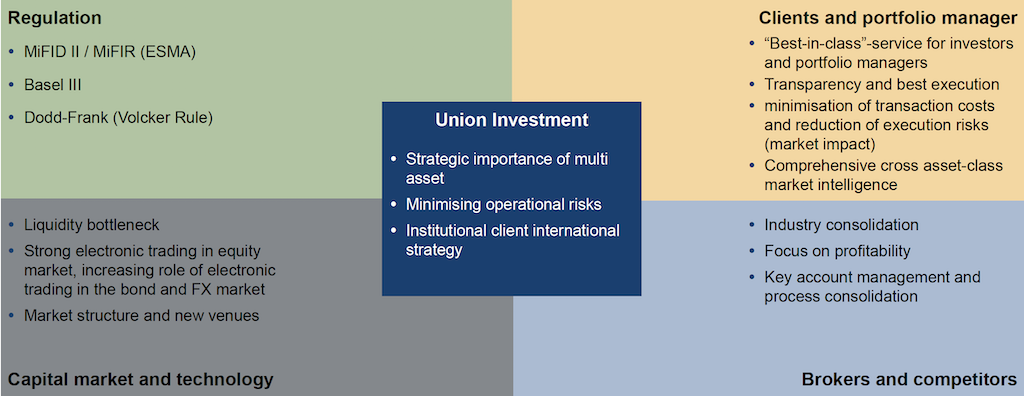

When I joined Union Investment we had initially two completely separate trading desks with very little interaction between the two. One desk was in charge of executing cash equity and derivatives transactions and the other executed fixed income and FX business. My task was to combine those two trading units but also to evolve that combined trading desk from being a pure executor of transactions to become a true service and solutions provider. When looking at the individual asset classes, there are lots of different features and characteristics but on the other hand there are also lots of similarities. Back in 2014, regulation was a key topic across all the asset classes and in that context, it also had a big impact on both technology and also on the availability of liquidity in financial markets. Taking these parameters into account we started defining one of our key targets, defining best-in-class execution across all the individual asset classes. In addition, we didn’t want to manage broker relationships by single asset classes only, ensuring that we as Union Investment are seen with a holistic view by broker firms and not as single and separate trading desks. These were the four key considerations when defining the strategy for our multi-asset trading desk: regulation, liquidity, best-in-class execution and managing broker relationships.

We believe that providing market intelligence is also a key part of our job

What benefits are achieved by getting your trading desk and portfolio managers working closer together?

Around 10 to 15 years ago, a trader on a buy-side trading desk was predominantly seen as someone who purely executes orders which are generated by portfolio managers. My philosophy is that we are actually a service and solutions function for the portfolio managers of Union Investment and our portfolio managers are seen as our “internal clients”, so to say. Therefore, we believe that providing market intelligence and advice around liquidity are also key parts of our job. It is as important as the execution business that we share this tactical-based knowledge and advice with our portfolio managers. Therefore setting up a multi-asset trading desk was a complete shift from offering a pure role as an execution desk to running a service and solution function which delivers the very best possible outcome for our internal clients, our portfolio managers, and also to our external clients, our end investors.

What are the key tasks and objectives of the central multi-asset trading desk of Union Investment?

In summary, it’s the delivery of best-in-class execution to our portfolio managers by accessing the best possible liquidity pools, by minimise market impact and slippage. That helps us to optimise both the implicit and the explicit cost of trading. Additionally the delivery of market intelligence on flows, positioning and sentiment and liquidity advice is highly relevant. It’s also important to “know your client”. Portfolio managers need to be treated differently and therefore require different services, which you need to understand as a trader to offer them the required services which adds real value.

Evolution in market structure and trading environment with big impact on how to deliver best-in-class execution to clients

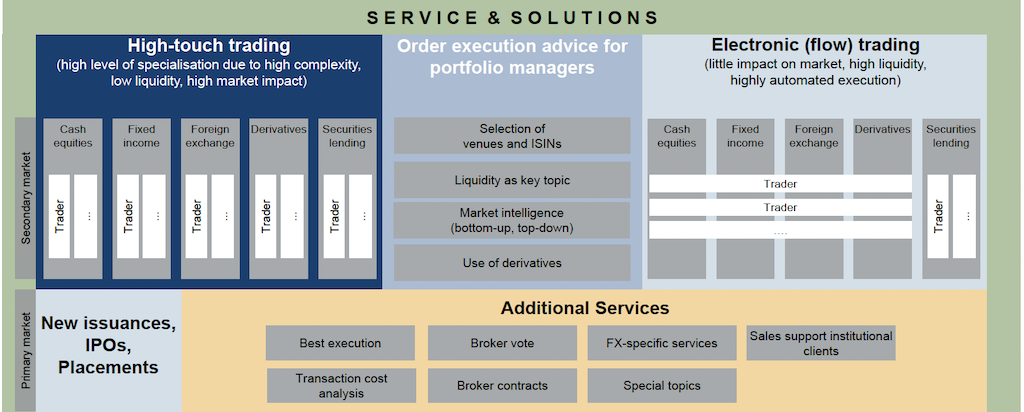

Please tell us a little about the range of services and solutions that your trading desk offers.

We have a centralised trading desk at Union Investment, so nearly all transactions in cash equities, fixed income instruments, FX and derivatives are executed by our trading desk. On top, securities lending for enhancing the performance of the portfolios to deliver additional alpha to our clients is also a key part of our trading desk offering. We also run a trading services function, some may call it middle office services, which is an integral part of our team.

What type of additional services do you offer which create added value for your portfolio managers?

Execution on a day to day business is core for us. Everything related to market intelligence is something I see as an additional value-add to our portfolio managers. In general our portfolio managers have a very in-depth, fundamental approach we are an active asset manager. Therefore, it’s of relevance from a tactical point of view that we share trading related thoughts about flows, positioning, sentiment and technicals. That’s where we come in as an advisor to our portfolio managers. That’s one part of what I consider as market intelligence. And the other part, as I mentioned previously, is more about advice where our team can see trends across the different asset classes and share those as recommendations to the portfolio managers, almost acting in a trading advisory function.

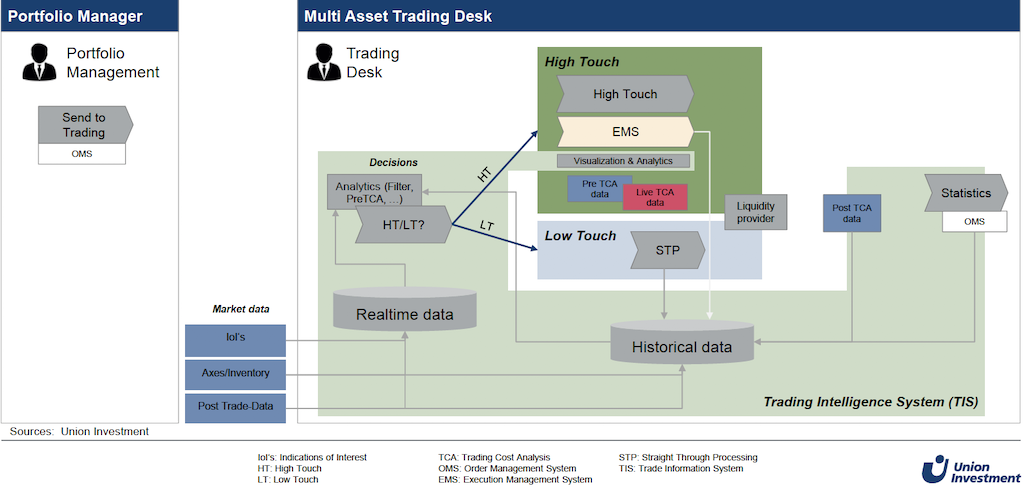

Ensuring that your team stays ahead of the curve in terms of technology is now a key determining factor in its success

Best execution is an integral part of the strategic goal of your multi-asset trading desk. How do you go about ensuring that it can deliver this in an environment where a mixture of high-touch and low-touch trading across asset classes is increasingly required?

From an organisational point going forward we look at two key determining factors – on the one hand liquidity and on the other hand technology. From my perspective, being able to address both factors in the best manner is really a key factor in defining the success of a trading desk. When looking at liquidity it’s essential that we take into account the various different types of orders we have and for each individual asset class we are connected to all relevant sources of liquidity which helps us to improve the execution quality, which helps us to achieve the very best outcome for our investors. On the other hand, technology is also highly important these days and a major driver of delivering best-in-class execution. For the last three years we had a number of big IT projects related to the multi-asset trading desk where topics like execution management systems, transaction cost analysis (TCA), automization, differentiation between high-touch and low-touch trading and data mining were addressed. Ensuring that your team stays ahead of the curve in terms of technology is now a key determining factor. It’s important to ensure that you have the highest level of true trader DNA in combination with intelligent technology – both critical for high-touch and low-touch trading.

You generate additional alpha across all asset classes and minimise execution costs by using sophisticated trading strategies. How do you leverage transaction cost analysis to help you achieve this?

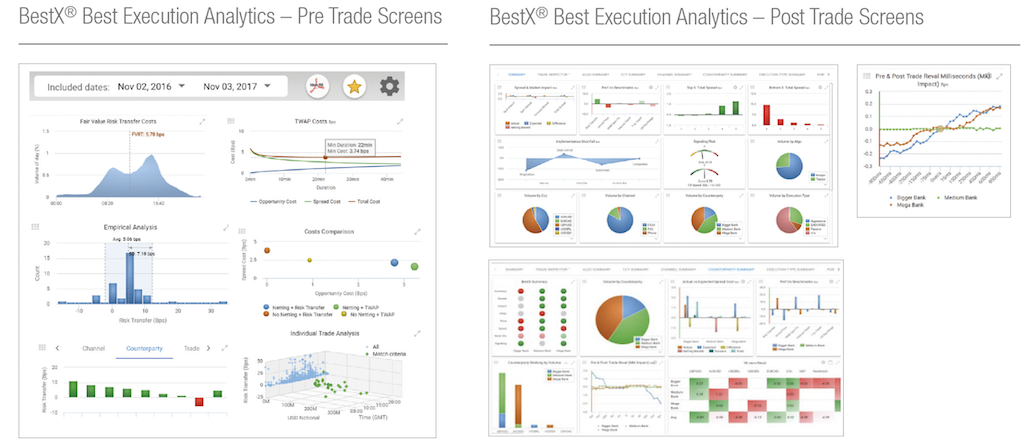

TCA is an important element across all asset classes. Originally it started years ago in the equities space where we have had initially a post-trade TCA on a parent order level in place. But as important as analysing the performance of quality of transactions after a trade is done is a sophisticated pre-trade TCA, a TCA during the live-time of the order. A post-trade TCA on a fill level shows you for each individual fill the quality and also toxicity and reversion around these transactions. A transaction cost analysis is therefore for sure not only an instrument used to prove best execution, so a box ticking exercise. It delivers much more information – it is a tool allowing you constantly to optimize your execution outcome.

There’s a lot to learn in FX from the experience of using algos in the equities space

Why is Pre-Trade Information combined with post-trade analysis so important in helping you to deliver best-in-class execution to clients?

Pre-trade analysis shows what your expected outcome of an execution for different ways of trading should be, so pre-trade TCA gives you a pretty good benchmark of where you should end up with your execution. Then by combining the outcome in post-trade TCA and comparing this to the pre-trade TCA this quantitative measure of alpha you are delivering to your investors. Additionally there are also lots of qualitative measurements but from a quantitative perspective your TCA is clearly key in determining your alpha generation.

Investment in trading intelligence is now seen as a key requirement by many leading asset managers. How does Union Investment go about leveraging FX data, analytics and statistics etc?

As I have mentioned, investing and building smart technology is really one of the success factors going forward. What we are working on is creating a trading information system – and that’s also something we will roll out for all asset classes – one big engine where we collect all the pre-trade and post-trade data, live and historical orders. This will help us further to improve broker selection, to improve selection of the various liquidity pools, to achieve optimizing our trading strategies. That’s all with the goal of achieving the very best outcome for our investors. You have to make sure that it’s not only about collect the data but that you make smart use of this raw data you collected.

Trading desk as “service & solutions desk” reflects the increasing market requirements for best execution

What do you see as the biggest challenges in trying to accurately compute execution metrics in FX?

It’s important to have the right data in place to determine an optimal trading style for each individual order. Based on all the smart data, historic volumes and volatilities and typical volume patterns during the course of the day it is about finding the very best strategy to minimise your market impact on the one hand. But it is also about taking the timing risk into account when, for instance, making use of algos where you typically have a longer period of trading compared to trading against risk transfer. That’s where you need highly sophisticated traders, well trained to in making decision such as defining the best way of executing for an individual order. Do you go for a request for quote, do you go for an algo, or is it a combination of both instruments? When going for RFQ, the question is what are the best brokers for this order to select. When going for an algo, what is the best algo strategy, what is the best broker algo accessing the best liquidity pools available? A key point is – and that’s applicable for both ways of trading – to minimize your footprint in the market, to minimize information leakage.

In what ways has the evolution in FX market structure impacted on how you deliver best-in-class execution to clients and has it encouraged you to explore new execution alternatives and methods to undertake them including FX algorithmic trading?

In the past, the predominant trading protocol was RFQ and most of the business was done via risk transfer with broker firms. Over the last couple of years we’ve had, not quite an equitisation of FX, but we’ve certainly seen certain equity-type trading styles being adopted, especially when looking at algos, which in the past were already used for decades in the equity space. Therefore, there could be some learning in FX from the expertise and experience of using algos in the equities space. With a broader usage of algos you have new brokerage firms, the alternative liquidity providers, coming up.

FX algos are a helpful addition for certain situations to enhance your execution quality. It is highly critical to have a full understanding of the functionality of algos and to be aware of the potential benefits they can deliver. But it is also necessary to know about who is participating in providing liquidity and measuring toxicity and reversion data to avoid being gamed. Therefore FX algos from our perspective are a beneficial addition to the ecosystem for helping to improve your execution quality but you need to be 100 percent sure about the functionality of the algos you are using.

Investment in trading intelligence as a key requirement: data, EMS, high touch/low touch, pre-, live- and post-trade TCA, statistics

How supportive of the FX Global Code has Union Investment been and in what ways does it help your efforts to deliver the highest standards for clients?

We are highly, highly supportive of the Code. Union Investment signed the Code back in November last year and we’re still among only a small group of asset managers who have signed up to show our commitment to the Code. To me it was a signal both internally but also externally to our investors underlining the message that we as Union Investment fulfil the highest quality standards in the execution across all asset classes, including the FX space.

In equities and fixed income, we have MiFID II which sets a basis for quality standards which we deliver to our investors, in derivatives it is EMEA, but we don’t have a similar “hard” regulation in the FX markets. Over the last five years we have set up structures where we can proudly say that we deliver best-in-class standards to our investors. That’s applicable for equities and fixed income and also derivatives. We are demonstrating by signing the Code that we fulfil those highest standards to our clients in FX as well.

In what ways do you try and utilise new and more innovative quantitative solutions to support best execution and market microstructure analysis with respect to FX?

I have highlighted before, that technology is a key driver for us and we believe that innovation is vital to stay ahead of that curve. Addressing with liquidity providers our expectations and highest standards in combination with our in-depth knowledge and structures, this delivers the very best outcomes for our end investors. Driving the evolution of market structure, having innovative and visionary thinking as a key element of our strategy and being part of major industry groups like the ECB’s FX Contact Group is really important for us to remain a leading firm in execution across all asset classes.

Pre-Trade Information in combination with post-trade analysis is key to deliver best-in-class execution to clients

Finally let’s talk specifically about FX algos. How long have your trading teams been utilising algorithmic execution in order to handle FX orders and what factors usually determine the type of algos they use and how they are sourced?

We as Union Investment have been an early user of broker algo technologies to optimize the quality of our executions. When looking at algos in general, not only in FX, the key difference compared to accessing a risk price is minimise market impact but you need to take into account longer times to get the execution done. Typically when going for a risk price, you have an immediate fill in combination with a bigger market impact. Making use of algos you have a longer period it takes to get the order filled, so you have a bigger time and volatility risk, but you can minimize your impact. Therefore a trader needs to be fully aware of the functionality of algo and its pros and cons. He needs to make the judgment call trade by trade whether he is better off with a risk price or using an algo to get the very best execution outcome. As a result, we would never use algos if we weren’t 100 percent sure about their functionality. From our perspective, an algo is not an instrument where you stick an order in and the algo will do everything for you. As a sophisticated trader you need to be the driver, proactively and constantly leading the process of executing orders when making use of this tool.

What are the important things you are trying to achieve when using algorithmic FX trading techniques?

At the end, it’s all about generating the very best outcome and maximizing the alpha you are generating for your end investors. And then it’s up to the trader to make use of the entire toolbox we have set up to access financial markets. It is his decision on a trade by trade basis which instrument to use to achieve this very best result. When using an algo, questions he needs to take into account are related to broker selection, are whether to make use of a passive or aggressive strategy, which proportion of the order to buy immediately and which proportion to run via an algo strategy. As a trader, it is essential that you are the active driver of all the decisions. You need constantly to monitor whether the outcome of using the algo is going in your expected direction. It is clearly not the case and this shouldn’t be your expectation that an algo is doing everything for you.

As a trading desk, you need to have an in-depth understanding of what you can achieve with algos and you need to have full transparency about the quality of the execution

Are there any specific things that you would like developers and providers of FX algos to put more focus on?

It is all about transparency, transparency and transparency. That’s what we expect from our partners who provide us with algos. As a trading desk, you need to have an in-depth understanding of what you can achieve with algos. You need to have full transparency about the quality of the execution. You need to know each individual timestamp of your fills. You need to know where you traded. You need to measure toxicity and reversion of the individual. All of that is essential to optimize your algo selection, your broker selection and selection of liquidity pools you are accessing.

There is not always a consistent correlation between the cost of one particular algo and the direct benefits it delivers. What would you like to see done to address that?

As a trader you need to be fully aware of the functionality and the execution quality which is delivered by the algo. In the end, you need a high level of quantitative data which is necessary to judge the outcome of the algos.

You and your team won the 2017 Leaders in Trading Award in the category ‘Buy-side multi-asset desk of the year’. How important are the use of new execution toolsets like FX algos likely to become in helping top class trading teams like yours to stay ahead in the future?

Being ahead of the curve and to remain ahead of the curve enables you and your team to deliver highest quality standards in execution to our investors. A well-thought strategy in combination with innovative visionary thinking is really key. That’s why in my opinion FX algos are an highly important piece of the whole execution landscape to achieve best-in-class execution for our investors. It’s an essential element of the toolbox we use when selecting trading strategies, when selecting liquidity pools, when selecting broker firms for getting the very best alpha outcome for our investors. Therefore working further on the development of smart algos is a vital part of the evolution of the FX space.